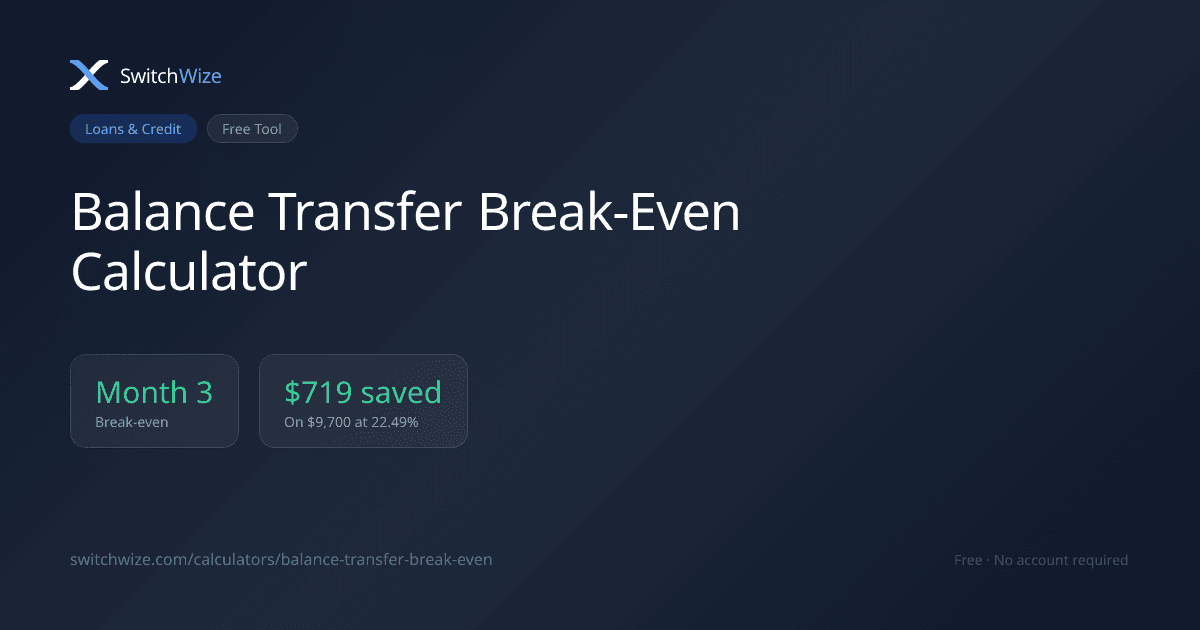

- A balance-transfer fee is prepaid interest, not a penalty. On a $9,700 balance at 22.49% APR, a 4% fee ($388) is offset by avoided interest by month three of an 11-month payoff, a net gain of $719.

- The fee is rarely the problem. The average card carrying a balance now charges 21.52% APR, about $2,152 a year per $10,000, so almost any transfer fee pays for itself within one to three months.

- Two offers can say '0% interest' and behave completely differently: a true 0% intro APR only charges interest going forward, while a deferred-interest offer retroactively charges the entire original balance if even one dollar is left when the promo ends. The CFPB has flagged this specifically.

- Divide your balance by the promo months before you apply. That figure is the minimum payment required to clear it in time; a break-even calculator can show your exact payoff month and total savings.

Quick answer

A 0% balance transfer is worth it when you clear the balance inside the promo window, and the fee itself is almost never why it fails. On a $9,700 balance at 22.49% APR, a 4% transfer fee costs $388 up front. Left on the original card at $1,000 a month, that same balance generates $1,107 in interest before it hits zero, which means the fee is fully offset by month three. Every month after that is money kept, not money saved on paper. The real risk sits somewhere else entirely: whether the offer is a true 0% APR or a deferred-interest offer that punishes a single missed dollar, and whether you actually clear the balance before the promo ends.

Megan is 42 and lives in Columbus, Ohio, and she ran this exact math before she did anything. She owed $9,700 on a card charging 22.49% interest, had already stopped using it, and could commit $1,000 a month to killing it. A new card offered her 12 months at 0%, with a 4% fee taken off the top. The offer felt backwards: hand over $388 in real cash today to move debt from one bank to another? She priced it out before she decided, and the fee lost that argument by the third month.

The fee is prepaid interest, so price it that way

A transfer fee is usually 3% for the first few months, then 5% on most major cards, and some charge a flat 5%. Stop reading it as a fee and read it as interest paid in advance. At the average 21.52% APR, every month you carry $10,000 costs about $179 in interest. A 3% fee is $300, roughly 1.7 months of interest. A 5% fee is $500, under three months' worth. On Megan's $9,700 balance at her actual 22.49% APR, the math is even more lopsided: a $388 fee versus a card that was going to cost her $1,107 in interest regardless.

That reframing tells you the breakeven almost instantly. If you would otherwise carry the balance longer than two or three months, the fee already pays for itself. On that test, nearly every transfer wins, which is exactly why the headline math is a distraction and the fine print underneath it is the real game.

Megan's numbers, worked in the open

Here is the full comparison, month by month, not just the summary. Megan's card charges $9,700 × 22.49% ÷ 12, or roughly $182 in interest the first month alone, tapering as the balance shrinks. Paying $1,000 a month, she is debt-free in 11 months, having paid $1,107 in interest along the way.

The transfer path adds the $388 fee to her balance, financing $10,088 at 0% for the promo. At the same $1,000 monthly payment, she clears it in just over 11 months, roughly the same payoff timeline, for a single $388 charge and nothing else.

Cost to hold, 1 years

$0 entry + $1,107/yr

$388 entry + $0/yr

Same payoff timeline, about 11 months either way. The only thing that changes is $719.

Both paths take her about the same 11 months to reach zero. One of them costs $1,107. The other costs $388. That gap, $719, is the entire case for transferring, and it exists whether or not Megan feels anxious about paying a fee she can see versus interest she can't.

The trap hiding in the fine print: deferred interest

Before Megan transferred anything, she checked one more thing most people skip: whether her offer was a true 0% intro APR or a deferred-interest offer. They read almost identically in an ad and behave completely differently on a statement.

A true 0% intro APR does exactly what it sounds like. If a balance survives past the promo, interest starts accruing going forward on whatever is left, and only on that amount. A deferred-interest offer, common on store cards and retail financing, works on a different clock entirely. If even a small balance remains when the promotional period ends, the issuer can reach back to day one and charge interest on the entire original amount financed, retroactively, as though the promotion never applied. The Consumer Financial Protection Bureau has specifically warned consumers about this structure on deferred-interest promotional financing.

The tell is buried in the Schumer Box, the standardized APR disclosure table every card offer is legally required to show. "0% Introductory APR" is the safer promise. "No interest if paid in full" is the deferred-interest signal, and it means the safety net disappears entirely if you fall even one dollar short.

Why careful people still walk into it

A monthly interest charge is a pain signal. It's calculated daily and billed quietly, but it still shows up on the statement every month as a number that stings a little. A 0% offer switches that signal off completely, so the same disciplined person who would have attacked a 22% balance suddenly feels no urgency against a 0% one. The fee, by contrast, is paid in one visible motion, which is exactly why it feels like the bigger cost even when the math says otherwise. Issuers understand this bias well. The promo is not a gift; it is a bet that you will still be carrying the balance when the rate resets, or that you'll trip the deferred-interest wire on a card that was never really offering 0% in the way you assumed.

Picture the version of this story where Megan skips the math: same offer, same $10,088 financed balance, but minimum payments only. By month 12, most of that balance is still outstanding right as the 0% window closes, and whatever card she chose reasserts its real APR (or, on a deferred-interest card, bills retroactive interest on the full amount). The $388 fee bought her nothing but a delay, and possibly a penalty on top of it.

What to actually do

- Divide before you apply. Balance divided by promo months is the payment required to win. Megan's financed balance was $10,088; over her self-imposed 11-month deadline (one month inside the actual 12-month promo, as a buffer), that's $917.09. She rounded up to $925 as her autopay floor and paid her full $1,000 whenever cash flow allowed.

- Check the Schumer Box before you apply. Look for "0% Introductory APR" explicitly. If the offer instead says "no interest if paid in full," you're looking at deferred interest, and a single missed dollar at the deadline can trigger retroactive charges on the whole balance.

- Do not spend on the new card. Purchases often are not covered by the 0%, and payments can be applied in ways that leave the expensive balance sitting there. Use it for the transfer and nothing else.

- Set a payoff alarm one month before the reset date, not the day of. The reset is the whole risk, so treat the date like a bill.

- Call your current issuer first. A June 2026 LendingTree survey found 84% of cardholders who asked for a lower APR got one, averaging a 6.3-point cut. On $10,000, dropping from 21.52% to 15.2% saves about $632 a year with no fee and no new account, and if you are going to pay slowly anyway, that can beat a transfer outright. Compare live balance-transfer offers only after you have done this.

The rules, stacked

- A transfer fee is not a fee. It is interest you prepaid, so price it in months.

- The 0% rate is never the question. The reset date is, and so is which kind of 0% you actually signed up for.

- Deferred interest is retroactive. A true 0% APR is not. Read the Schumer Box before you apply, not after.

- If you cannot name the monthly payment that clears the balance in time, you do not have a plan. You have a deferral.

- The cheapest 0% offer is the one you have already paid off before anyone reminds you it existed.

Does the math work for you?

| Situation | Best next move | Why |

|---|---|---|

| You can commit to balance / promo months every month | Transfer | The fee costs less than a few months of interest you are avoiding. |

| Your offer says "no interest if paid in full" | Read the terms twice, then decide | That phrasing signals deferred interest; a missed deadline charges retroactive interest on the full balance. |

| The required payment is out of reach | Ask your issuer for a lower APR first | Most who ask get a cut, with no fee and no new account. |

| You would pay minimums either way | Skip the transfer | The fee buys a delay, and the go-to rate is often higher than your current one. |

| Multiple balances across cards | Move the one you can kill in time | A partial transfer you clear beats a full transfer you cannot. |

Run your own numbers

Megan's math works because her numbers happen to clear the fee by month three. Yours might break even in month one or month nine, depending on your balance, your APR, and the fee on the table, and that number is worth knowing before you apply, not after.

For context, the average card APR tracked on this site currently sits at 24.00%, so every month a balance survives past the reset costs real money. If card debt is one of several fires, Money Map shows which to put out first.

Sources

- Federal Reserve G.19 Consumer Credit release for the average APR on accounts assessed interest (21.52%, early 2026).

- LendingTree credit-card APR study (June 2026) for the share of cardholders who obtained a lower APR by asking.

- Consumer Financial Protection Bureau consumer guidance on deferred-interest promotional financing.

- NerdWallet, CNBC, and WalletHub balance-transfer roundups (June 2026) for intro lengths up to 21 months and 3%-then-5% fee structures.

Megan is a composite character; the dollar figures are representative and current as of June 2026. Educational only, not individualized financial advice.

Frequently Asked Questions

Is a balance transfer worth it?

How do I calculate the balance-transfer breakeven?

What is the catch with 0% APR transfers?

What is deferred interest, and how is it different from a true 0% APR balance transfer?

Act on this: today's top balance transfer

Ranked by SwitchWize's composite score. We may earn a referral fee, and it never changes the ranking order.

Editorial review

What changed since the last update

Was this guide helpful?