- The $6 coffee debate is useful only up to a point: visible spending gets noticed first, but invisible account gaps can be just as expensive.

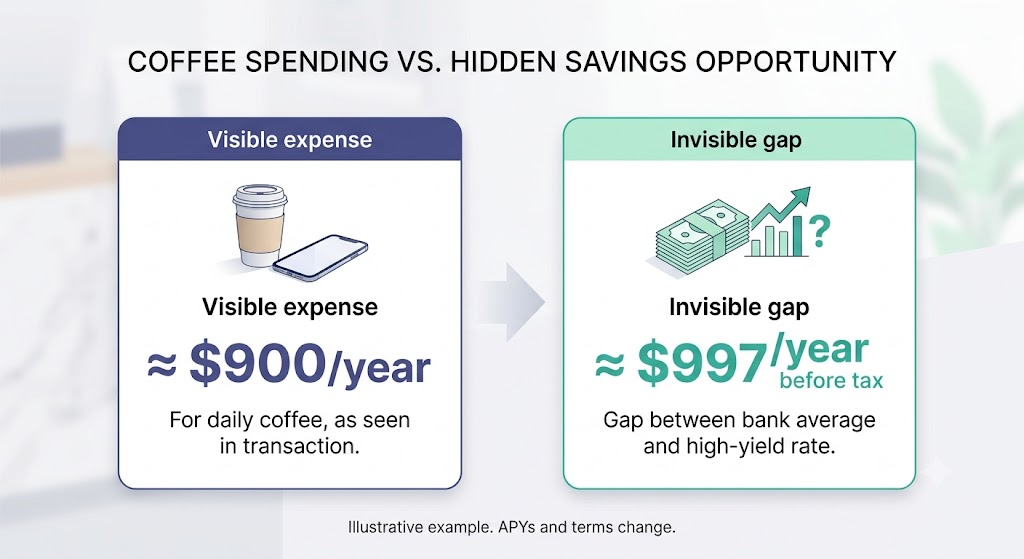

- A $25,000 savings balance earning 0.38% instead of 4.37% creates an illustrative gap of about $997.50 a year before taxes.

- Before cutting the small parts of life you actually enjoy, check for gaps that are invisible, unwanted, and fixable.

The coffee is easy to notice.

It shows up as $6.18 after tax. It appears in the banking app almost immediately. It comes with a cup, a lid, a little cardboard sleeve, and that familiar budget voice that arrives before the first sip.

Was that necessary?

Not panic. Not real regret. Just the small pinch of having spent money on something that was not strictly required.

A lot of personal finance advice lives inside that moment. It points at the coffee, the lunch, the delivery order, the extra streaming service, the ride-share, the small thing you bought because the day was long and you wanted one part of it to feel easier.

And sometimes the advice is right.

Small spending does add up. If you buy a $6 coffee three times a week for 50 weeks, that is $900 a year.

That is real money.

If the purchase is automatic, joyless, or crowding out something you care about more, it deserves a look. SwitchWize is not here to pretend small purchases do not matter.

But the coffee has one unfair advantage.

You can see it.

The coffee gets a receipt. It gets a line item. It gets a moment of guilt. It gets remembered because you chose it with your own hand and watched the money leave.

A money gap does not work that way.

A money gap can sit inside an account that looks perfectly fine. The app opens. The balance is there. Nothing flashes red. The transfer button works. Your emergency fund is still your emergency fund.

So you close the app.

Nothing happened.

That is the trick.

Some money leaks do not look like spending. They look like nothing happening.

Discipline and inertia can look the same

A savings account earning very little does not feel like buying coffee. It does not feel like buying anything.

It feels like safety. It feels like adulthood. It feels like the responsible thing you already handled years ago.

You opened the account. You put money there. You left it alone.

That sounds disciplined.

And sometimes it is.

But discipline and inertia can look almost identical from the outside.

One is a choice you keep making on purpose. The other is an old choice that keeps making itself because life got busy and no one asked you to revisit it.

That is why the small expense gets blamed first.

The coffee interrupts your day. The bank gap does not. The lunch shows up on your card. The low APY hides in the background. The weekend dinner feels optional. The old savings account feels neutral.

But neutral is not always free.

This is where guilt becomes a bad ranking system.

Guilt is good at finding the thing you touched most recently. It is not good at finding the thing costing you the most.

It will point at the coffee because the coffee happened today. It will point at the dinner because the dinner was visible. It will point at the shoes, the concert, the takeout, the small purchase with a story attached to it.

It may completely miss the account that has been quietly under-earning for years.

That does not mean the small purchase does not matter.

It means the order of blame may be wrong.

The bank gap hides because it feels normal

Guilt is strangely bad at finding waste. It is much better at finding pleasure.

That is why people often attack the part of spending that has a face.

The coffee. The dinner. The trip. The thing that made the week feel a little more human.

The invisible product setting gets away with more because it does not feel like a decision. It feels like background.

And background does not usually make people feel guilty.

This is one reason old accounts survive. They are not just accounts. They are proof that you did something responsible once.

You needed a place for savings, so you opened one. You needed an emergency fund, so you built one. You needed financial stability, so you chose safety over risk.

That decision may have been right.

But old responsible decisions can become stale without becoming obviously wrong.

The account still works. The money is still there. The bank still recognizes you. The app still opens.

Nothing feels broken.

So nothing gets checked.

But "working" and "working well" are not the same thing.

The math can change the story

Take a simple example.

Suppose someone has $25,000 in emergency savings. It is sitting in a savings account earning 0.38% APY, the national savings-rate level shown by FRED's FDIC-linked savings-rate series for June 2026. If a high-yield alternative earns about 4.37% APY, the gap is 3.99 percentage points.

On $25,000, that difference is about $997.50 a year before taxes.

| Input | Example value |

|---|---|

| Savings balance | $25,000 |

| Current APY | 0.38% |

| Comparison APY | 4.37% |

| APY gap | 3.99 percentage points |

| Estimated annual gap | $997.50 before taxes |

The math is not complicated:

4.37% - 0.38% = 3.99 percentage points

$25,000 x 3.99% = $997.50

That number is not a promise. APYs change. Account terms matter. Interest can be taxable. Some accounts have balance limits, minimums, transfer timing, or other requirements. Emergency money still needs to be liquid, accessible, and held at an institution that fits your needs.

The highest number on a page is not automatically the best account for a real household.

But the example changes the conversation.

The first question is no longer, "Should I feel bad about coffee?"

The better question is, "Where is the biggest unwanted, invisible, fixable gap in my financial life?"

That question is calmer. It is also more useful.

Because a lot of people do not need another lecture about small spending. They already know small spending adds up. They have heard the coffee speech. They have done the mental math. They have opened the banking app after a purchase and felt the tiny sting.

What they may not have done is rank the problem.

They may not have compared the cost of a small habit with the cost of an old account. They may not have checked whether their emergency fund is safe but underpaid. They may not have asked whether a money decision that once made sense still fits today's rate environment.

And that is not because they are careless.

It is because financial products are quiet when they become stale.

The expensive thing is not always the loud thing

A bad subscription nags you once a month. A low savings rate rarely announces itself. A high credit card APR only becomes obvious when the balance carries. A mortgage rate feels like old paperwork until the payment starts to feel heavy. A checking account fee feels normal if it has been there long enough.

The expensive thing is not always the thing that makes the most noise.

Sometimes the expensive thing is the thing that became part of the furniture.

This is why "just cut back" can feel so unsatisfying. It asks people to start with sacrifice before diagnosis. It turns personal finance into a character test instead of a ranking problem.

But not every dollar has the same emotional value.

A coffee that gets you through a hard morning is not the same as an avoidable account gap. A dinner with friends is not the same as a forgotten fee. A trip you will remember for years is not the same as cash sitting in the wrong place by habit.

Some spending is part of the life you are trying to build.

Some leakage is just leakage.

The goal is not to defend every purchase. The goal is to stop treating guilt as the map.

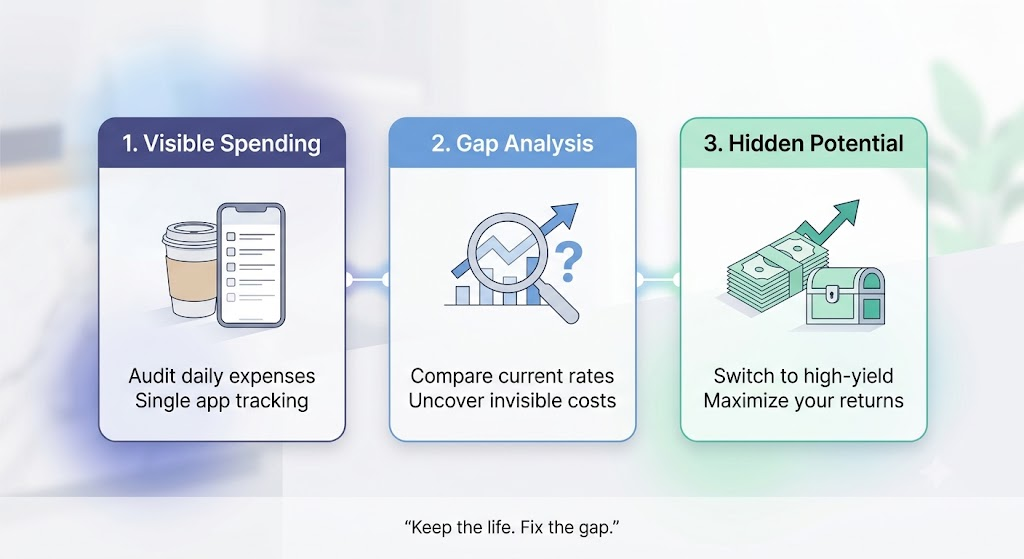

Start with gaps that are invisible, unwanted, and fixable

A better ranking system starts with three tests.

First, is the gap invisible?

You are not already feeling it every day. It does not come with a receipt, a notification, or a moment of obvious regret.

Second, is the gap unwanted?

It is not buying joy, time, safety, access, convenience, or anything you consciously value.

Third, is the gap fixable?

You can compare options, understand the tradeoff, and make a reasonable move without rebuilding your entire financial life.

A low-rate savings account can pass all three tests.

So can avoidable fees. So can a stale credit card setup. So can a loan you never revisited. So can an account that was right for who you were ten years ago but not for how you use money now.

This does not mean you should chase every decimal point.

That can become its own kind of waste.

If two accounts are close, convenience may matter more. If the money is for emergencies, access matters. If you use branch services, cash deposits, linked transfers, or family account features, those are real considerations.

The point is not to optimize until life becomes smaller.

The point is to check whether the thing you are cutting is actually the thing costing you.

A better tool does not begin by asking what you can give up.

It begins by asking what you would gladly fix if the number were clear.

How SwitchWize fits

That is where SwitchWize fits.

Run Money Map to see which money decision may be worth checking first. It can help you compare hidden gaps across savings, debt, cards, mortgage, and other money decisions before you start cutting the small things that make life feel better.

Before you cut the coffee, check the gap.

If the coffee is automatic and meaningless, cut it.

But if it is one of the small things that makes your day feel human, do not start there just because it is easy to see.

Start with the silent gap.

The one without a receipt.

The one you would gladly fix if someone showed you the number.

What to Do Now

Related reading

- Savings Account Rate Gap Calculator Guide

- Should You Switch Savings Accounts in 2026?

- Where to Keep Your Emergency Fund

- The State of the Rate Gap

- Why the National Average Savings Rate Can Mislead You

Frequently asked questions

Is buying coffee bad for my budget?

Not automatically. Small purchases can add up, but the point is to compare them against larger invisible gaps before assuming they are the main issue.

What is a bank gap?

A bank gap is the difference between what your current account gives you and what a realistic alternative could offer, after considering rates, fees, access, terms, and safety.

How do I calculate a savings-rate gap?

Multiply your balance by the difference between your current APY and the alternative APY. For example, a 3.99 percentage point gap on $25,000 is about $997.50 before taxes.

Should I always move money to the highest-yield savings account?

No. APY matters, but so do FDIC or NCUA insurance, account access, transfer timing, balance limits, fees, minimums, and your own need for liquidity.

Is emergency savings different from regular savings?

Yes. Emergency savings should usually prioritize safety and access. A higher APY is useful only if the account still fits the role of emergency money.

Sources and verification

| Claim | Source | Verified |

|---|---|---|

| National savings rate was 0.38% for June 2026 | FRED National Rate: Savings, sourced from FDIC data | 2026-06-26 |

| FDIC publishes national deposit rates and caps | FDIC National Rates and Rate Caps | 2026-06-26 |

| SwitchWize HYSA calculator referenced a 4.37% top available rate | SwitchWize HYSA Calculator | 2026-06-26 |

| Best high-yield savings offers materially exceed the national average | SwitchWize Savings Rate Watch | 2026-06-26 |

Editorial disclosure

This article is educational and illustrative. It is not personalized financial, tax, legal, or investment advice. APYs, fees, product terms, and availability can change. Readers should verify account terms, insurance coverage, liquidity, tax treatment, and suitability before moving money.

SwitchWize may earn referral fees from some providers. That does not change our editorial framing, calculator logic, or organic article recommendations.

Frequently Asked Questions

Is buying coffee bad for my budget?

What is a bank gap?

How do I calculate a savings-rate gap?

Should I always move money to the highest-yield savings account?

Is emergency savings different from regular savings?

Answer a few questions about your situation and goals. Money Map points you to the highest-value next step across savings, mortgage, cards, and debt.

Editorial review

What changed since the last update

Was this guide helpful?